Introduction

In 1994, financial planner William Bengen published research that changed the way Americans think about retirement income. Instead of asking only how large a portfolio should be, he asked a more useful question: how much could a retiree withdraw each year, adjust that amount for inflation, and still have a high likelihood of not exhausting the portfolio over a long retirement?

The result became known as the 4% Rule. It suggested that a retiree beginning with a balanced portfolio of stocks and bonds could withdraw about 4% of the starting portfolio value in the first year, then increase that dollar amount each year for inflation, and historically survive every 30-year period Bengen tested. For personal finance learners, the rule matters because it connects saving, investing, spending, inflation, and longevity into one understandable framework.

The 4% Rule also became central to the financial independence movement. If a household can estimate its annual spending, it can approximate the portfolio required to support that spending by multiplying annual expenses by 25. A household spending $40,000 per year would target roughly $1,000,000; one spending $80,000 would target roughly $2,000,000. The rule is not a guarantee, but it gives learners a powerful starting point.

Background

Bengen's research used historical U.S. market data to study retirement periods beginning in different years. He examined portfolios made up primarily of large-company U.S. stocks and intermediate-term government bonds, then tested how different withdrawal rates would have performed across past market sequences. The key innovation was not simply calculating an average return, but examining sequence-of-returns risk: the danger that poor market returns early in retirement can permanently damage a portfolio.

The study focused on a 30-year retirement horizon, which is a practical planning period for many traditional retirees. A person retiring at 65 may need money to last into their 90s, and a couple may need to plan around the longer life expectancy of the surviving spouse. Bengen tested constant real withdrawals, meaning the retiree took the same purchasing power each year rather than reducing withdrawals after bad markets.

The research built on a core reality of retirement planning: retirees face uncertainty from several directions at once. Investment returns fluctuate, inflation erodes purchasing power, and lifespan is unknown. Bengen was trying to identify a withdrawal rate that had survived even difficult historical periods, including retirements that began before the Great Depression, before high inflation in the 1970s, or before long bear markets.

Findings & Lessons

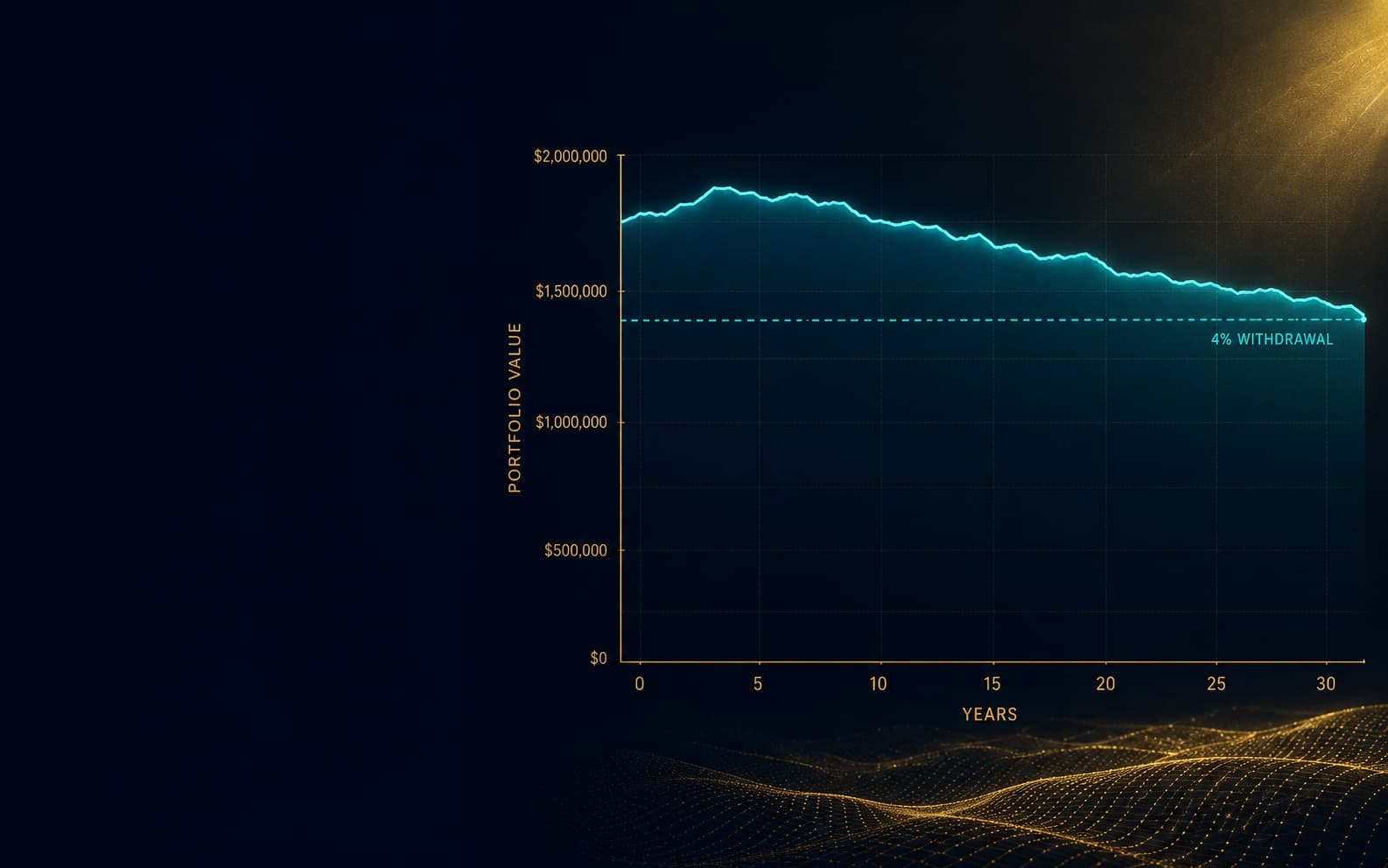

The central finding was that a first-year withdrawal rate of about 4% of the starting portfolio, followed by inflation adjustments, historically allowed a balanced stock-and-bond portfolio to last at least 30 years in every period Bengen examined. In practical terms, a retiree with $1,000,000 could withdraw $40,000 in the first year. If inflation were 3%, the second-year withdrawal would rise to $41,200, regardless of whether the market had gone up or down.

The lesson is that average returns can be misleading. A portfolio may earn a reasonable average return over 30 years but still fail if the worst losses occur early, when withdrawals are simultaneously removing capital. This is why sequence matters. A retiree who experiences a severe bear market in the first five years is in a very different position from one who experiences the same bear market after 20 years of strong returns.

The 4% Rule also shows why asset allocation matters. A portfolio that is too conservative may not grow enough to offset inflation over decades, while a portfolio that is too aggressive may expose the retiree to painful short-term losses. Bengen's work supported the idea that retirees often need meaningful stock exposure even after leaving the workforce.

Implications & Application

For today's personal finance learner, the 4% Rule is best used as a planning estimate rather than a rigid command. It helps translate future spending into a target portfolio. If someone expects to spend $60,000 per year in retirement from investments, the rule suggests a target of about $1,500,000. If Social Security, a pension, or rental income covers $20,000 of that spending, the portfolio only needs to support the remaining $40,000, lowering the estimated target to $1,000,000.

A concrete example makes the idea clearer. Suppose Dana is 45 and wants to become financially independent by 60. She estimates that she will need $70,000 per year in retirement spending. She expects Social Security later, but she wants her portfolio to carry the full amount at first. Using the 25-times rule, her rough financial independence number is $1,750,000. This number gives her a savings target and helps her evaluate whether her current savings rate is enough.

The rule also encourages flexibility. A retiree does not have to withdraw mechanically every year. Many people reduce discretionary spending after market declines, use cash reserves temporarily, delay major purchases, or take part-time income. These adjustments can improve the odds of success. The deeper application is not "always spend exactly 4%," but "understand the relationship between spending, portfolio size, inflation, and market risk."

Historical Context

Bengen's work appeared during the 1990s, a decade when defined contribution plans such as 401(k)s were becoming increasingly important. Earlier generations often relied more heavily on employer pensions, but responsibility for retirement planning was shifting toward individuals. Workers had to decide how much to save, how to invest, and how to turn a portfolio into income.

The research also came before the long bull market of the late 1990s had fully reshaped investor expectations. Bengen's historical testing included much harsher periods than the recent past at the time, which made the research valuable. It reminded planners that retirement strategies should not be built only around optimistic assumptions or recent performance.

What It Teaches

The 4% Rule teaches that retirement planning is mostly about matching spending to sustainable assets. Investment returns matter, but spending rate is the lever that determines whether a portfolio is likely to last. A modest lifestyle can require dramatically less capital than a high-spending one.

It also reinforces probabilistic thinking. Personal finance is not about finding a perfect number that removes uncertainty. It is about making reasonable assumptions, building margins of safety, and staying flexible when reality differs from the plan. The rule gives learners a disciplined starting point while reminding them that no historical rule can eliminate future risk.

Key Concepts

Relevance Today

The 4% Rule remains relevant because retirees still need to convert uncertain investment portfolios into reliable income. Higher longevity, changing bond yields, inflation shocks, and early retirement goals all make the rule worth revisiting carefully rather than applying blindly.